Restaurant Financing in 2026: A Practical Owner’s Guide

Last Updated: June 17, 2026

Most restaurants don’t fail during a slow month. They fail after making a bad financial decision during a busy one.

A second location becomes available. The kitchen needs a full equipment overhaul. The operation is losing orders, and table turns because there’s no restaurant management system in place.

These sound like hypothetical problems, but they’re not. They are the exact inflection points where you seek outside funding and take the first option that says yes.

That’s where things go wrong.

Restaurant financing is a spectrum of processes with very different costs, timelines, and risk profiles.

This guide covers all 10 financing options—loans, lines of credit, equity, and everything in between—with the requirements, real costs, and honest trade-offs for each.

The goal is not to tell you which option to take. It’s to give you clarity to make the call yourself.

What is restaurant financing?

Restaurant financing is any form of outside capital to support business needs that daily cash flow cannot cover, including opening a new location, renovating space, upgrading restaurant technology or equipment, and scaling operations or expanding.

This is secured through either debt (loans that must be repaid) or equity (investment in exchange for ownership).

Having financing for your restaurant directly determines your business’s ability to operate consistently, respond to change, and grow sustainably.

This means it can solve unstable cash flow, enabling you to grow at the right time, which directly impacts your profitability.

But more so, financing can turn into a competitive advantage for your business to expand faster than competitors and invest in systems that improve margins, such as restaurant order management systems, automation, inventory, and the like.

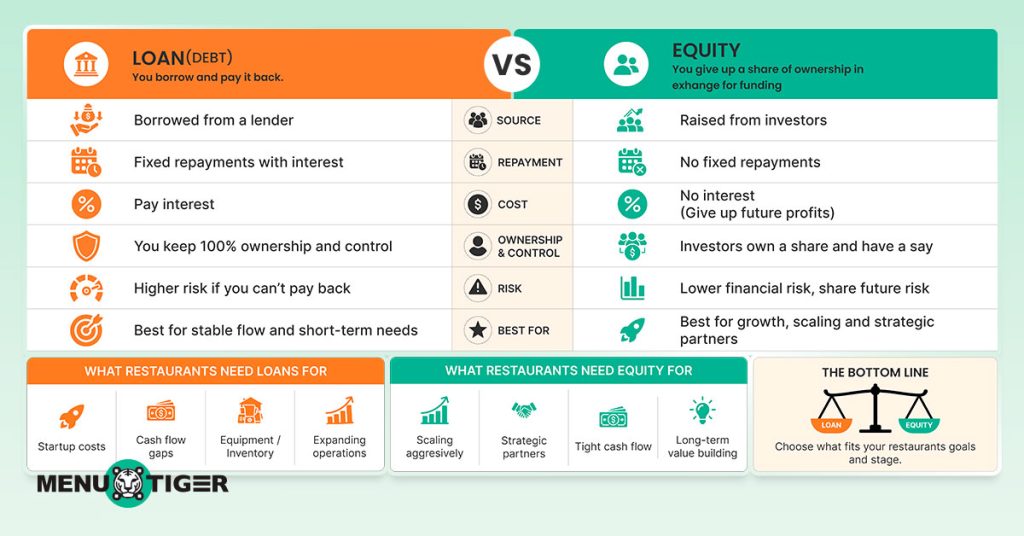

Loan vs. equity: Which is best for you?

Restaurant financing comes in two forms.

Debt financing (loan) means borrowing a principal amount from a lender—a bank, financing firms, or private investor—with the agreement of repaying over a set term with interest, and retaining full ownership of your restaurant.

Equity funding, on the other hand, means raising capital by giving up a share of ownership in your business instead of borrowing it.

Unlike in loans, there’s no need for you to repay on a fixed schedule.

Instead, investors provide the capital (the amount you need) in exchange for a stake in your restaurant and a share of future profit.

Restaurants often use equity if their cash flow is tight for loan repayments, or they want to scale aggressively, or they just want to find strategic business partners.

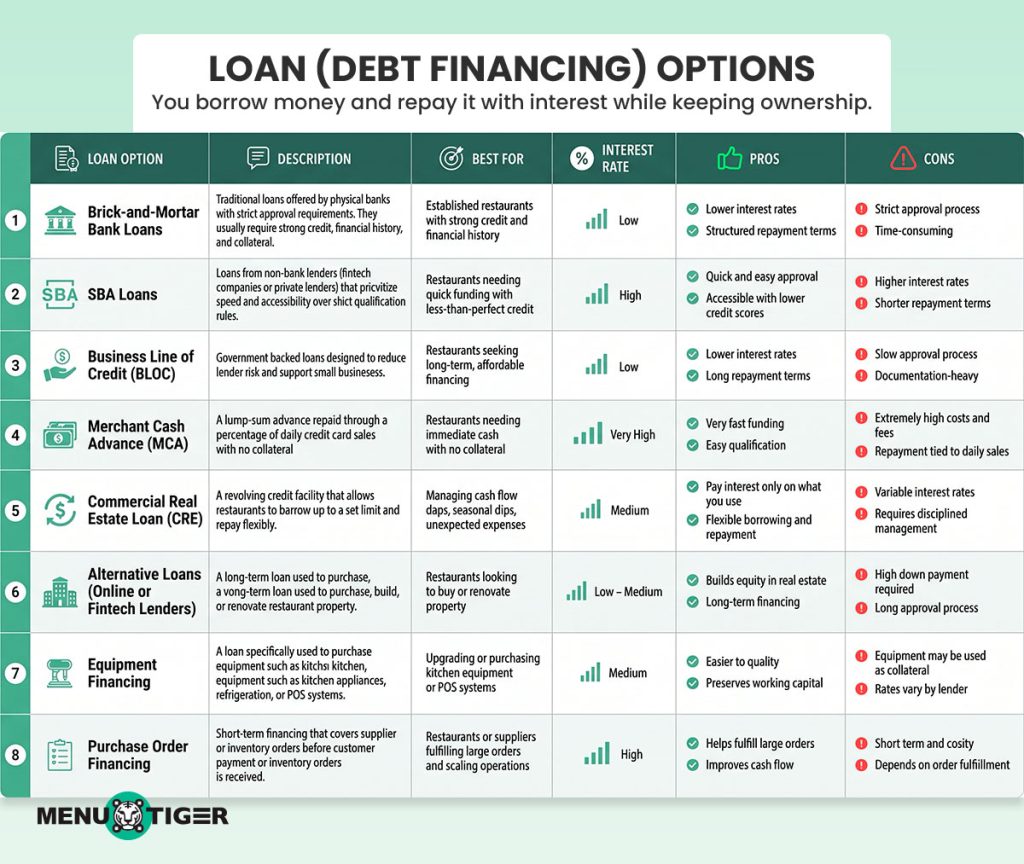

8 loan-based restaurant financing options

You keep full ownership but must repay with interest.

1. Brick-and-mortar loans

This traditional business loan from the bank or credit union is used to finance physical restaurants that want to open a new location, expand, or renovate existing dine-in startups.

It’s popular among full-service restaurant business models, cafes, and franchise operators that are scaling or just want to improve their physical spaces.

Typical requirements:

- Business must have at least 2 to 3 years of operating history

- Stable revenue and strong credit

- financial records (tax returns, business and personal financial statements)

- A business plan

- Down payment or collateral

| Pros | Cons |

| Low interest rates (around 6%–10%) help reduce long-term borrowing costs. | A slow approval process can delay access to funds. |

| Offers larger loan amounts for major business needs or expansion | Requires extensive paperwork and documentation. |

| Provides longer repayment terms for manageable monthly payments | Qualification can be difficult due to stricter requirements. |

2. SBA loans

Small Business Administration (SBA) loans are provided by government-backed lending partners in the United States to help small business owners to access financing with lower risks for the lenders.

Instead of lending directly, the SBA loan program will take a portion of the full amount.

For example, on a $100,000 SBA loan, the SBA might guarantee 75% of the balance.

This means the lender carries full risk only for the remaining $25,000.

In its simplest takeaway, the government promises the bank that it will cover part of the loss if the borrower fails to repay.

Typical requirements:

- Business eligibility (operating in the US; small business under SBA standards)

- Credit requirements ( 650+ personal credit score with few defaults or bankruptcies in credit history)

- Operating for at least 2 years

- Financial documents (Personal and Business tax returns, Profit & loss statements, cash flow, balance sheet

- Business plan

- Down payment (usually around 10% to 20% of the total project cost

- Collateral (a personal guarantee from the owner is required)

- Legal documents (Business registration, licenses and permits, and lease agreement)

| Pros | Cons |

| This business loan for small businesses usually offers lower interest rates compared to private financing. | Difficult to qualify due to stricter eligibility requirements. |

| Provides longer repayment terms (typically 10–25 years). | Requires strong credit, complete financial documents, and a solid business plan. |

| Lower monthly repayments help improve cash flow management. | The approval process is often slow and paperwork-heavy. |

| Suitable for businesses seeking stable, long-term funding. | Many lenders require a personal guarantee and sometimes collateral, increasing owner risk. |

3. Business Line of Credit (BLOC)

A Business Line of Credit gives operators access to a set borrowing limit.

Unlike a term loan, where you receive a lump sum and begin repaying immediately, a BLOC lets you draw only what you need, pay interest only on the amount drawn, and replenish the available credit as you repay.

For example, if you are approved for a $50,000 line of credit and only need $10,000 to buy ingredients and cover payroll, you can withdraw the amount you need and be charged interest for that amount only.

Once repaid, the amount will be added to your remaining credit.

Typical requirements:

- Credit score (Usually 600 ot 680+ minimum, higher credit score, higher chance for approval

- 6 months to 2 years of operating history

- Proof of steady monthly or annual revenue

- Financial documents (bank statements for 3 to 12 months, tax returns, and basic profit and loss records

- Business bank account

- Business registration

- Personal guarantee

| Pros | Cons |

| Provides flexible access to cash when needed. | Interest rates are usually higher than those of traditional loans. |

| The approval process is generally faster and easier. | New businesses may face even higher rates or stricter terms. |

| Useful for managing short-term operational expenses. | Credit limits are often lower and may not cover large expenses or expansion costs. |

4. Merchant Cash Advance (MCA)

A Merchant Cash Advance (MCA) is a type of business financing where the restaurant receives a lump sum of cash in exchange for a percentage of its future sales.

Repayment is automatic and fluctuates based on how much you earn each day.

For example, a $20,000 advance with a 1.3% factor rate means repaying $26,000 total.

Instead of paying monthly, the provider takes 10% (can vary depending on providers) of the restaurant’s daily card sales.

This means if you make $1,000 in sales a day, $100 goes toward repayment.

Typical requirements:

- Common sales volume (at least $5,000 to $10,000 per month in daily credit/debit sales)

- At least 3 to 6 months of operating history

- Business bank statements (Usually for 3 to 6 months to show cash flow)

- Active payment processing (Restaurant order system or POS terminal)

- Business registration

| Pros | Cons |

| Fast approval process with quicker access to funds. | Highly effective interest costs can make it an expensive financing option |

| Minimal requirements and less paperwork compared to traditional loans. | Daily sales deductions may negatively impact restaurant cash flow. |

| Approval is often based on sales performance, not just credit score. | Can become difficult to manage during slower sales periods. |

5. Commercial Real Estate Loan (CRE)

A Commercial Real Estate (CRE) loan finances the purchase, construction, or major renovation of establishments instead of leasing a space.

It’s a long-term loan with repayment periods ranging from 10 to 25 years, depending on the lender’s structure.

Restaurant owners go for CRE to gain full control of their location, build equity, and avoid rising rental costs, which makes it a stable move for established businesses.

Typical requirements:

- High credit score (around 680 to 720+ for stronger approval chances

- Down payment (typically 20% to 30% of the property price

- Business financial statements

- Debt service coverage ratio (DSCR) (Usually around 1.20+, meaning the restaurant earns enough to comfortably cover loan payments)

- At least 2 years of operation

- Property appraisal

- Business plan (if expanding or new purchase)

- Legal documents

| Pros | Cons |

| Offers low interest rates (around 5%) compared to many other financing options | Requires a large upfront down payment (typically 20%–30%). |

| Longer repayment terms help keep monthly payments more manageable. | Qualification often requires strong credit and a solid financial history. |

| Suitable for businesses looking for stable, long-term financing. | Approval standards are strict and heavily based on business performance. |

| Can support major investments such as property or large assets. | Property value may significantly affect approval and loan terms. |

6. Alternative loans (Online or Fintech lenders)

Alternative lenders—online platforms or fintech companies—evaluate restaurants differently from regular banks.

Approval decisions draw on cash flow, sales, and bank activity rather than a strict credit history.

For restaurants that need working capital quickly and do not have a profile for a bank or SBA loan yet, this is the most practical fast-access option.

Typical requirements:

- Operating history of 3 to 12 months

- Monthly revenue ( often at least $8,000 to $15,000 in consistent sales)

- Credit score (depending on the lender)

- Active business bank account

- Basic business information

| Pros | Cons |

| Fast approval process, often providing funding within days. | Usually comes with higher interest rates than traditional loans. |

| Flexible qualification requirements make it easier to access. | Shorter repayment terms can result in higher regular payments. |

| Accessible for restaurants with limited credit history or less documentation. | May create tighter cash flow pressure due to more expensive repayment schedules. |

7. Equipment financing

Equipment financing funds specific asset purchases—ovens, refrigerators, dishwashers, self-service kiosk, POS terminal, or a restaurant management system.

The equipment serves as collateral, which is why approval is faster and less credit-intensive than general business loans for big and small businesses.

Payments are fixed and monthly, making it one of the more predictable financing structures available.

Typical requirements:

- Credit score (preferably high, but lower may still qualify with higher cost)

- Often, 6 to 12 months of minimum operation

- Revenue

- Equipment quote/ invoice

- Business documents (bank statement for 3 to 6 months)

- Down payment (0% to 20%, depending on the credit and lender

| Pros | Cons |

| Approval is often easier since the restaurant kitchen equipment itself serves as collateral. | Can become more expensive over time because of additional interest fees. |

| Fixed monthly payments make repayment more predictable and easier to budget. | Loan terms and approval may depend heavily on the type, condition, and value of the equipment. |

| Helps businesses acquire essential equipment without high upfront costs. | Missing a payment may result in losing the financed equipment. |

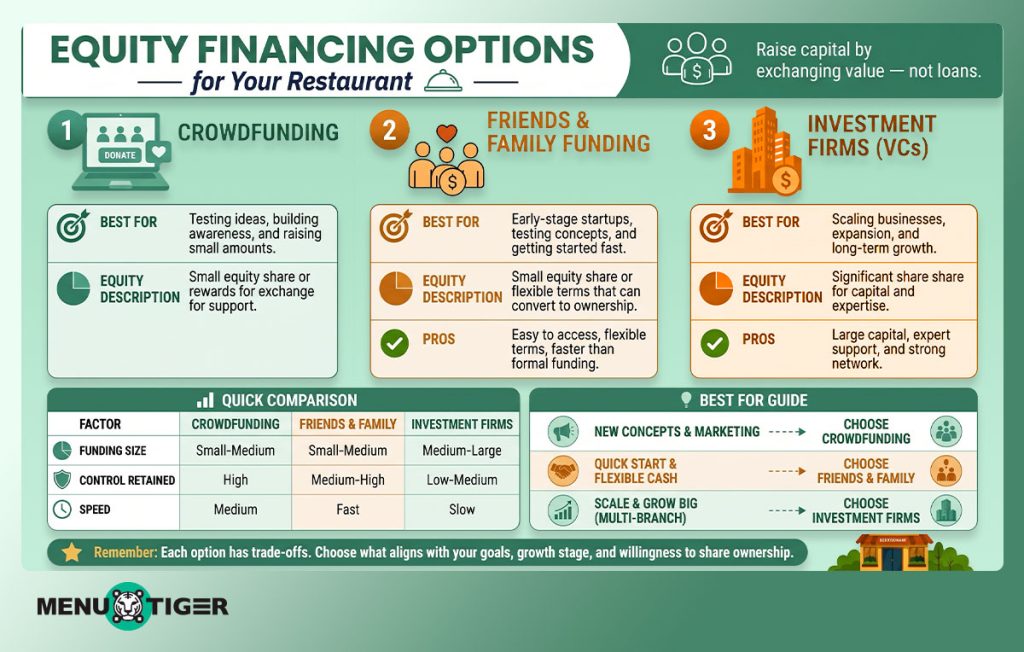

3 equity funding options

You don’t repay money, but you give up ownership and future profits.

8. Business crowdfunding

This is another alternative way to raise capital from a large number of people, or what is termed as ‘crowd’, and it’s usually done through online platforms.

Unlike the traditional move to take a loan from a bank, in crowdfunding, you collect small contributions from individuals who believe in your business idea.

You can either go for reward-based, where people participating can receive merchandise, discounts, or other rewards.

This option lets contributors have 1% of a share in your business.

How to apply:

- Provide a business plan

- Prepare campaign materials (Pitch video or story and marketing visuals)

- Financial and legal requirements (Bank account, identity verification, and business registration)

| Pros | Cons |

| Allows businesses to raise capital without taking on traditional debt. | Funding success is not guaranteed and depends on campaign performance. |

| Avoids high-interest payments and fixed loan obligations. | Requires strong marketing and promotion to attract backers. |

| Can help validate and test a restaurant concept early. | Marketing efforts may involve high upfront costs. |

9. Friends and family funding

This is an informal funding source where you can raise money from people you know to help you start a business.

The fund may be given as a first-time business loan to be repaid over the agreed period or as an investment in exchange for ownership or future returns.

No significant requirements needed, but make sure to create a restaurant business plan for their perusal so they’ll have the knowledge of what their funding is for.

| Pros | Cons |

| Usually, more accessible than traditional bank loans. | Can create personal risk if repayment is delayed or the business struggles. |

| Often has little to no strict requirements, credit checks, or a formal approval process. | May strain relationships with friends, family, or personal lenders. |

| Can offer more flexible repayment terms compared to formal financing. | Lack of formal legal structure may lead to misunderstandings or disputes. |

| Faster access to funding due to simpler arrangements. | Terms may be unclear if expectations are not documented properly. |

10. Investment firms

These are companies that provide capital to businesses in exchange for ownership or a share in future profits rather than requiring a repayment loan.

So, instead of lending money, they invest in your business because they expect it to grow and become more valuable over time.

Because they are more focused on growth potential, it’s necessary to prepare the following:

- Scalable concept (the restaurant model can expand into multiple branches, franchise potential)

- Proven traction (existing sales, strong customer demand, and successful pilot location

- Business plan

- Financial documents (Revenue data, margins, and projections)

- Experienced team

- Equity offer (willingness to give up a percentage of ownership in exchange for funding)

- Legal structure ( the business is properly registered)

| Pros | Cons |

| Provides access to large amounts of funding for growth or expansion. | Requires giving up partial ownership of the restaurant. |

| No monthly loan repayments, helping preserve business cash flow. | Restaurant investors may gain influence over business decisions or management rights. |

| Some investors bring industry expertise, mentorship, and valuable connections. | High expectations for growth and returns can create pressure to scale quickly. |

| Can support long-term expansion without increasing debt obligations. | Business goals may shift to align with investor priorities. |

How to choose the right restaurant financing for your business

Choosing the wrong financing structure is not just an expensive mistake—it is an operational one. The steps below give operators a practical framework for making a defensible decision before signing anything.

Define the exact use of funds before choosing a product.

Different financing types are built for specific use cases and do not function as a general funding source.

Be specific: is the capital for renovation, buying new kitchen equipment, or expanding your business?

The answer to that question will largely determine the most appropriate product.

Match the financing to your real use case.

Opening a new restaurant? SBA or bank loans offer long-term and low-interest rates.

Planning to add an online ordering software to your operation? Apply for equipment financing. It’s asset-backed and offers low interest rates as well.

Aligning what you need to the type of funding can prevent you from repayment strain.

Tip: You may seek advice from restaurant consultants to guide you on what type of financing can suit your business well.

Assess your repayment capacity honestly.

Lenders look at cash flow, credit score, time in business, collateral, and industry risk.

Most long-term and short-term business loans are either cheap but hard to acquire, or easy but expensive.

Understanding this dynamic helps you to make a realistic assessment, among the options you can access.

Apply where you genuinely qualify—not where you hope to

Applying to lenders whose threshold your profile doesn’t meet wastes time and generates hard credit inquiries. Don’t go for financing just because it’s available. In practice, easy approval often signals higher risk and higher cost.

This way, it can help you prevent short-term decisions, especially in an industry like this where margins leave little room for error.

The right financing decision starts with the right questions

Owners sometimes fall into unavoidable debt due to mismatched funding options.

The most effective approach to restaurant financing is to research and choose an option that directly supports how your business brings out revenue-driven outcomes, whether that’s improving efficiency or scaling demand.

Strategic investments, such as upgrading operations with a restaurant ordering system, can directly impact sales and customer experience, making financing easier to justify and sustain.

In the end, the right choice isn’t about accessing capital but more so about ensuring every cent borrowed works toward stronger and more predictable growth.

FAQs

Chevy

Before joining MENU TIGER's Content Team, Chevy has been dabbling in literary arts for five years, specifically creative writing in a theatre company. She loves exploring her creativity through painting, photography, and contemporary dancing.

Affiliates

© 2026 Menu Tiger. All rights reserved